Delta Hedging

This notebook compares delta hedging against simulated data with constant or stochastic volatility.

[1]:

from collections import defaultdict

from dataclasses import dataclass

from datetime import date

from decimal import Decimal

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import QuantLib as ql

from yabte.backtest import (

ADFI_AVAILABLE_AT_CLOSE,

ADFI_AVAILABLE_AT_OPEN,

Book,

CashTransaction,

OHLCAsset,

OrderSizeType,

PositionalOrder,

SimpleOrder,

Strategy,

StrategyRunner,

)

from yabte.utilities.simulation.geometric_brownian_motion import gbm_simulate_paths

from yabte.utilities.simulation.heston import heston_simulate_paths

Black Scholes Asset & Simple Delta Hedge Strategy

[3]:

# TODO: track call premium mtm valuation using constant / stochastic volatility

class QlBsm:

"""Black Scholes Model Pricer"""

def __init__(

self, K: float, sigma: float, exp: date, r: float = 0, S: float | None = None

):

self.option = ql.EuropeanOption(

ql.PlainVanillaPayoff(ql.Option.Call, K),

ql.EuropeanExercise(ql.Date().from_date(exp)),

)

day_counter = ql.ActualActual(ql.ActualActual.ISDA)

calendar = ql.NullCalendar()

self.S = S = ql.SimpleQuote(S or K)

self.r = r = ql.SimpleQuote(r)

self.sigma = sigma = ql.SimpleQuote(sigma)

risk_free_curve = ql.FlatForward(0, calendar, ql.QuoteHandle(r), day_counter)

volatility = ql.BlackConstantVol(

0, calendar, ql.QuoteHandle(sigma), day_counter

)

process = ql.BlackScholesProcess(

ql.QuoteHandle(S),

ql.YieldTermStructureHandle(risk_free_curve),

ql.BlackVolTermStructureHandle(volatility),

)

engine = ql.AnalyticEuropeanEngine(process)

self.option.setPricingEngine(engine)

def calc(

self,

t: date,

S: float | None = None,

sigma: float | None = None,

r: float | None = None,

greeks: bool = False,

) -> float | tuple[float, float, float, float]:

ql.Settings.instance().evaluationDate = ql.Date().from_date(t)

if S is not None:

self.S.setValue(S)

if sigma is not None:

self.sigma.setValue(sigma)

if r is not None:

self.r.setValue(r)

if greeks:

return (

self.option.NPV(),

self.option.delta(),

self.option.gamma(),

self.option.vega(),

)

else:

return self.option.NPV()

@dataclass(kw_only=True)

class BSMOption(OHLCAsset):

"""Black Scholes Model Option"""

K: float

exp: date

r: float = 0

divr: float = 0

cp: int = 1

def data_fields(self):

dfs = super().data_fields()

dfs.append(

(

"IVol",

ADFI_AVAILABLE_AT_CLOSE | ADFI_AVAILABLE_AT_OPEN,

)

)

return dfs

def intraday_traded_price(self, asset_day_data, size) -> Decimal:

ts = asset_day_data.name

bsm_option = QlBsm(K=self.K, sigma=asset_day_data.IVol, exp=self.exp, r=self.r)

price = bsm_option.calc(t=ts, S=asset_day_data.Close)

return round(Decimal(price), self.price_round_dp)

class DeltaHedgingStrat(Strategy):

def init(self):

# capture some data for analysis

self.metrics = defaultdict(dict)

def on_open(self):

data = self.data

p = self.params

ts = self.ts

# buy option on t0

if len(data) == 1:

self.orders.append(SimpleOrder(asset_name="CO_ACME", size=1))

# buy delta hedge shares

t = (p.exp - ts).days / 100

s = data.ACME.Open.iloc[-1]

vol = data.iloc[-1].loc["ACME"].IVol

bsm_option = QlBsm(K=p.K, sigma=vol, exp=p.exp, r=p.r)

_, delta, gamma, vega = bsm_option.calc(t=ts, S=s, greeks=True)

self.orders.append(

PositionalOrder(

asset_name="ACME", size=-1 * delta, size_type=OrderSizeType.QUANTITY

)

)

self.metrics[ts]["delta"] = delta

self.metrics[ts]["gamma"] = gamma

self.metrics[ts]["vega"] = vega

self.metrics[ts]["vol"] = vol

self.metrics[ts]["price"] = s

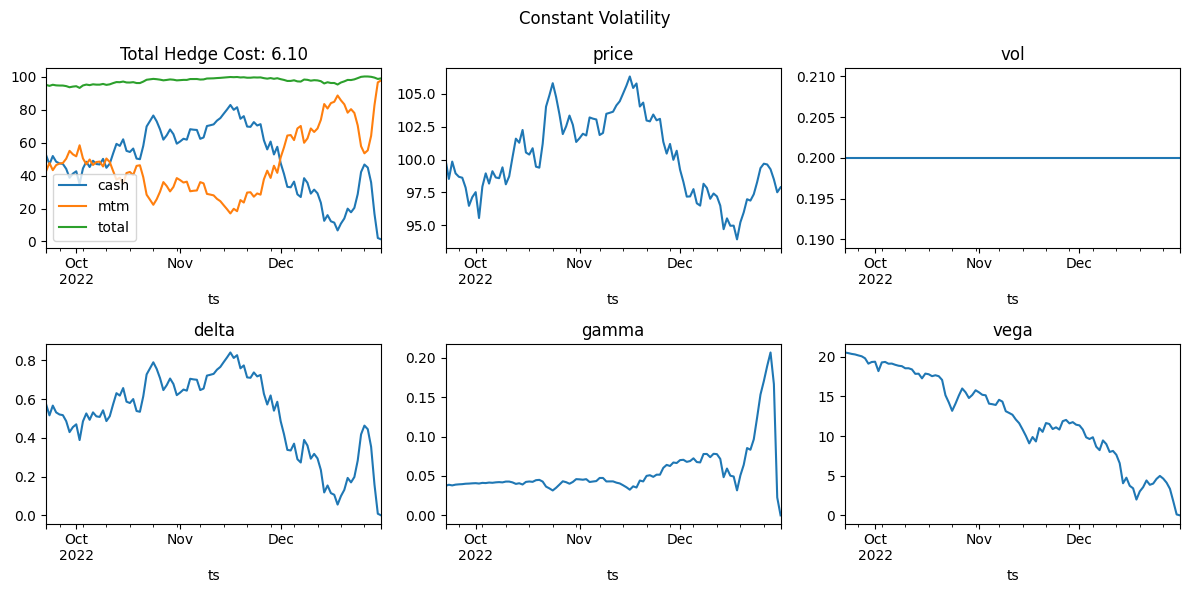

Constant Volatility

[4]:

# gbm params

r = 0.05

vol = 0.2

s0 = 100

N = 101

T = N / 365

# simulate data

rng = np.random.default_rng(12345) # for reproducibility

ix = pd.date_range(end="20221231", periods=N, freq="D")

p = gbm_simulate_paths(S0=s0, mu=r, sigma=vol, R=1, T=T, n_steps=N, n_sims=1, rng=rng)

df = pd.DataFrame(np.c_[p[:, :, 0], p[:, :, 0]], index=ix)

df.columns = pd.MultiIndex.from_tuples((("ACME", "Open"), ("ACME", "Close")))

# add constant vol to data

df.loc[:, ("ACME", "IVol")] = vol

# assets

assets = [

OHLCAsset(name="ACME", denom="USD", quantity_round_dp=6),

BSMOption(name="CO_ACME", data_label="ACME", K=s0, exp=ix[-1], r=r),

]

# run simulation

book = Book(name="Main", cash="0", rate=0.05 / 100)

sr = StrategyRunner(

data=df,

assets=assets,

strategies=[DeltaHedgingStrat()],

books=[book],

)

srr = sr.run(

{

"r": r,

"vol": vol,

"exp": ix[-1],

"K": s0,

}

)

metrics = pd.DataFrame.from_dict(srr.strategies[0].metrics, orient="index").reindex(

srr.book_history.index

)

[5]:

fig, axs = plt.subplots(2, 3, figsize=(3 * 4, 2 * 3))

fig.suptitle("Constant Volatility")

thc = srr.transaction_history[1:].total.sum()

srr.book_history.Main.plot(ax=axs[0][0], title=f"Total Hedge Cost: {thc:.2f}")

metrics.price.plot(title="price", ax=axs[0][1])

metrics.vol.plot(title="vol", ax=axs[0][2])

metrics.delta.plot(title="delta", ax=axs[1][0])

metrics.gamma.plot(title="gamma", ax=axs[1][1])

metrics.vega.plot(title="vega", ax=axs[1][2])

fig.tight_layout()

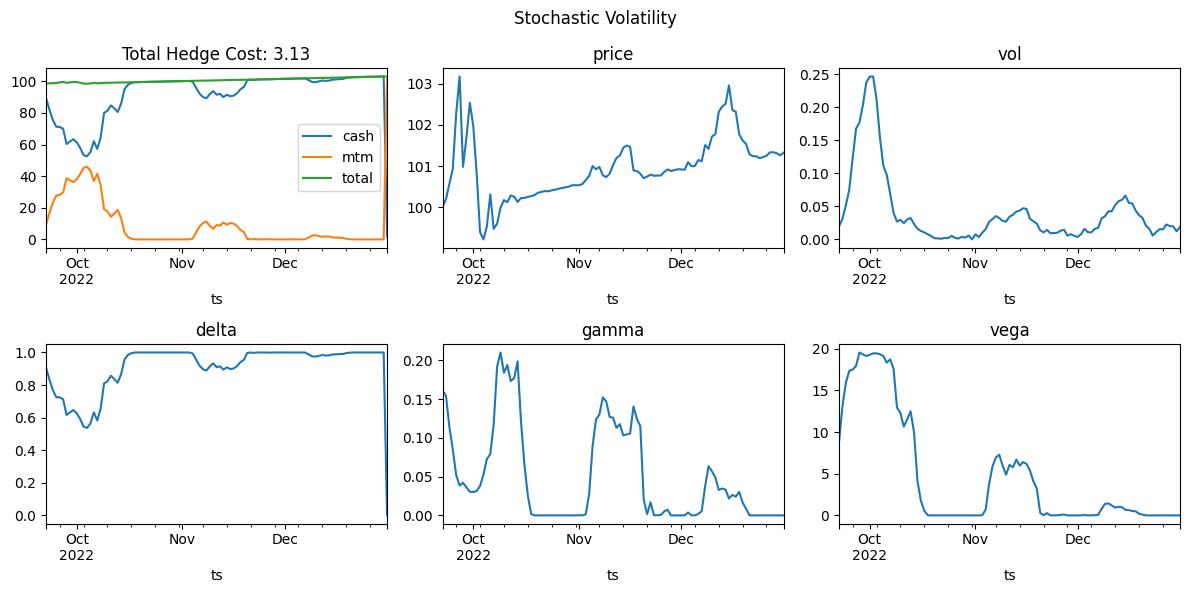

Stochastic Volatility

[6]:

# gbm params

r = 0.05

vol = 0.2

s0 = 100

N = 101

T = N / 365

kappa = 4

theta = 0.02

v0 = 0.02

sigma = 0.9

R = 0.9

# simulate data

rng = np.random.default_rng(12345) # for reproducibility

ix = pd.date_range(end="20221231", periods=N, freq="D")

p, vol = heston_simulate_paths(

S0=s0,

v0=v0,

mu=r,

kappa=kappa,

theta=theta,

xi=sigma,

R=np.array([[1, R], [R, 1]]),

T=T,

n_steps=N,

n_sims=1,

rng=rng,

)

df = pd.DataFrame(np.c_[p[:, 0], p[:, 0]], index=ix)

df.columns = pd.MultiIndex.from_tuples((("ACME", "Open"), ("ACME", "Close")))

# add constant vol to data

df.loc[:, ("ACME", "IVol")] = vol

# assets

assets = [

OHLCAsset(name="ACME", denom="USD", quantity_round_dp=6),

BSMOption(name="CO_ACME", data_label="ACME", K=s0, exp=ix[-1], r=r),

]

# run simulation

book = Book(name="Main", cash="0", rate=0.05 / 100)

sr = StrategyRunner(

data=df,

assets=assets,

strategies=[DeltaHedgingStrat()],

books=[book],

)

srr = sr.run(

{

"r": r,

"vol": vol,

"exp": ix[-1],

"K": s0,

}

)

metrics = pd.DataFrame.from_dict(srr.strategies[0].metrics, orient="index").reindex(

srr.book_history.index

)

[7]:

fig, axs = plt.subplots(2, 3, figsize=(3 * 4, 2 * 3))

fig.suptitle("Stochastic Volatility")

thc = srr.transaction_history[1:].total.sum()

srr.book_history.Main.plot(ax=axs[0][0], title=f"Total Hedge Cost: {thc:.2f}")

metrics.price.plot(title="price", ax=axs[0][1])

metrics.vol.plot(title="vol", ax=axs[0][2])

metrics.delta.plot(title="delta", ax=axs[1][0])

metrics.gamma.plot(title="gamma", ax=axs[1][1])

metrics.vega.plot(title="vega", ax=axs[1][2])

fig.tight_layout()

Transactions

[8]:

with pd.option_context("display.max_rows", None):

display(srr.transaction_history.head(20))

| ts | total | desc | quantity | price | asset_name | order_label | book | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2022-09-22 | -1.4100 | buy CO_ACME | 1.00 | 1.41 | CO_ACME | NaN | Main |

| 1 | 2022-09-22 | 90.55420000 | sell ACME | -0.905542 | 100.00 | ACME | NaN | Main |

| 2 | 2022-09-22 | 0.045 | interest payment on cash 89.14 | NaN | NaN | NaN | NaN | Main |

| 3 | 2022-09-23 | -90.72625298 | buy ACME | 0.905542 | 100.19 | ACME | NaN | Main |

| 4 | 2022-09-23 | 83.40617120 | sell ACME | -0.832480 | 100.19 | ACME | NaN | Main |

| 5 | 2022-09-23 | 0.041 | interest payment on cash 81.87 | NaN | NaN | NaN | NaN | Main |

| 6 | 2022-09-24 | -83.72251360 | buy ACME | 0.832480 | 100.57 | ACME | NaN | Main |

| 7 | 2022-09-24 | 77.19642573 | sell ACME | -0.767589 | 100.57 | ACME | NaN | Main |

| 8 | 2022-09-24 | 0.038 | interest payment on cash 75.38 | NaN | NaN | NaN | NaN | Main |

| 9 | 2022-09-25 | -77.47275777 | buy ACME | 0.767589 | 100.93 | ACME | NaN | Main |

| 10 | 2022-09-25 | 73.19413321 | sell ACME | -0.725197 | 100.93 | ACME | NaN | Main |

| 11 | 2022-09-25 | 0.036 | interest payment on cash 71.14 | NaN | NaN | NaN | NaN | Main |

| 12 | 2022-09-26 | -74.17314916 | buy ACME | 0.725197 | 102.28 | ACME | NaN | Main |

| 13 | 2022-09-26 | 74.12998700 | sell ACME | -0.724775 | 102.28 | ACME | NaN | Main |

| 14 | 2022-09-26 | 0.036 | interest payment on cash 71.14 | NaN | NaN | NaN | NaN | Main |

| 15 | 2022-09-27 | -74.78228450 | buy ACME | 0.724775 | 103.18 | ACME | NaN | Main |

| 16 | 2022-09-27 | 73.48366102 | sell ACME | -0.712189 | 103.18 | ACME | NaN | Main |

| 17 | 2022-09-27 | 0.035 | interest payment on cash 69.87 | NaN | NaN | NaN | NaN | Main |

| 18 | 2022-09-28 | -71.91684522 | buy ACME | 0.712189 | 100.98 | ACME | NaN | Main |

| 19 | 2022-09-28 | 62.26871112 | sell ACME | -0.616644 | 100.98 | ACME | NaN | Main |

[ ]:

[ ]: